A NEW CONTRIBUTION SYSTEM FOR THE SELF-EMPLOYED WAS APPROVED IN 2023 IN SPAIN.

Under the new approved Law by Real Decreto-ley 13/2022 of July 26th 2022, individuals who start their self-employment activity and register as self-employed from January 1, 2023, must report all the activities. Additionally, those who are already registered as of January 1, 2023, and engaging in more than one self-employed activity, are also required to report all their activities to the General Treasury of the Social Security.

HOW CAN I MAKE REPORT MY ACTIVITY TO SOCIAL SECURITY?

Both the registration in the Special Regime for Self-Employed Workers and the communication of such activities can be completed through Importas, the Portal of the General Treasury of the Social Security.

At Marfour International law firm, one of our English-Speaking accountants can take care of this process on your behalf.

What does this Royal Decree-Law 13/2022 of July 26th, 2022, modify and what are its most relevant points?

HOW WILL I CALCULATE THE PAYMENT OF MY AUTONOMOUS CONTRIBUTION TO THE SOCIAL SECURITY?

1. Since the law’s approval, All self-employed persons will pays social Security contributions on the basis of their annual net income obtained in the course of all their economic, business or professional activities, with the exception of individuals except persons who are members of a religious institution belonging to the Catholic Church will not pay contributions.

HOW WILL THE CONTRIBUTION BASE WILL BE CALCULATED IT?

The contribution base, defined as the total net income obtained in the calendar year from various, in the exercise of their different professional or economic activities, will be taken into account. This includes activities, regardless of whether they are carried out individually or as partners or members of any entity, with or without legal personality, as long as they do not have to be registered as employees or similar. The net computable yield for each activity carried out will be calculated according to the provisions of the IRPF rules, with specific variations depending on the group to which they belong.

For further information, please consult one of our immigration lawyers or Spanish accountants at Marfour International Law Firm.

HOW MUCH I CAN I REDUCE IN TERMS OF GENERAL EXPENSES?

A deduction of 7 percent for general expenses will be applied to the resulting amount, except in cases where the self-employed worker possesses the following characteristics, in which case the percentage will be 3 percent:

1. Administrator of capitalist mercantile companies with a participation of 25 percent or more.

2. Partner in a capitalist mercantile company with a participation of 33 percent or more.

This is general information that should be adapted to your personal situation by your personal Spanish accountant.

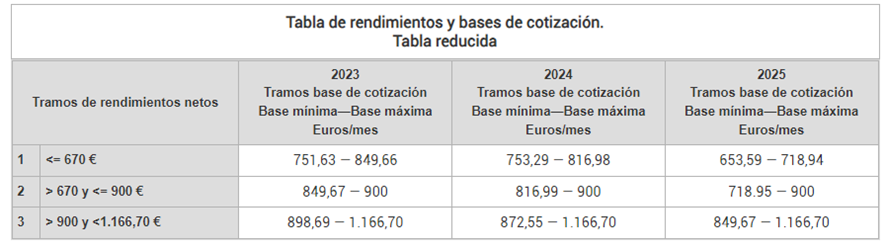

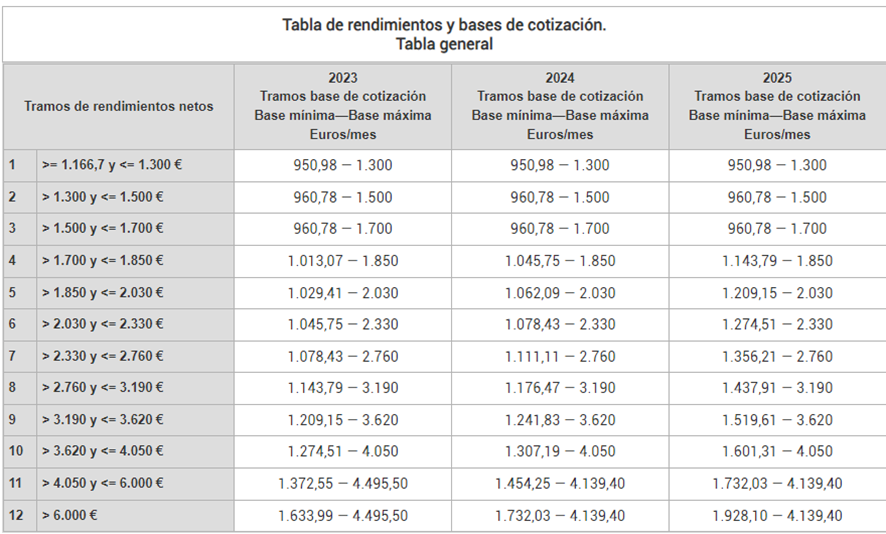

TABLE OF CONTRIBUTIONS BASED ON THE OBTAINED INCOME

1. How much will I pay according to my annual income?

The General State Budget Law will establish general and reduced tables of contribution bases. These will be divided into consecutive brackets of net monthly income amounts, with each bracket being assigned maximum and minimum monthly contribution bases.

The following table shows these new income brackets and their corresponding contribution bases for the next three years

2. Can I change my contribution base?

If during 2023 you predict a variation of net income, it will be possible to select, every two months, a new contribution base. A new quota would be applied, with a maximum of six changes per year. This modification will be effective on the following dates:

• March 1, 2023, if the request is made between January 1 and the last calendar day of February.

• May 1, 2023, if the request is made between March 1 and April 30.

• July 1, 2023, if the application is made between May 1 and June 30.

• September 1, 2023, if the application is made between July 1 and August 31.

• November 1, 2023, if the application is made between September 1 and October 31

• January 1, 2024, if the application is made between November 1 and December 31.

3. What I must I do if my total income is lower than I expected or higher?

There is a system to regularize social security contributions.

The monthly contribution bases selected each year will remain provisional until the annual regularization of the contribution is carried out.

If the tax continuation selected during the year is lower than that associated with the income reported by the corresponding Tax Administration, the employee will be notified of the difference of the amount.

If the contribution exceeds the maximum base of the income bracket, the Treasury will reimburse the difference before April 30 of the fiscal year following the year in which the contribution was made.

IS THERE A FLAT RATE FOR NEW SELF-EMPLOYED INDIVIDUALS?

During the period 2023-2025, individuals who newly register as self-employed may request the application of a reduced fee (flat rate) of 80 euros per month during the first 12 months of activity. The application will be made at the time of registration, with a possibility of extension.

For more information, please consult our immigration lawyers or accountants at Marfour International Law Firm. Do does not hesitate to get a consultation with one of our immigration lawyers in Spain.

Please note that blog content may be updated over time pending changes in the law or administrative practices. We recommend seeking professional advice based on your individual circumstances.